Plan Your Study Loan

A study/Educational loan, also known as a student loan, is a type of loan that is designed to help students finance their education. These loans are typically offered by government agencies, Government banks, private banks and other financial institutions. The purpose of a study loan is to provide students with the necessary funds to pay for tuition fees, textbooks, and other educational expenses. The terms and conditions of study loans vary depending on the lender and the type of loan.

Some Popular Loans are below:

IDFC first bank- Education Loan in India

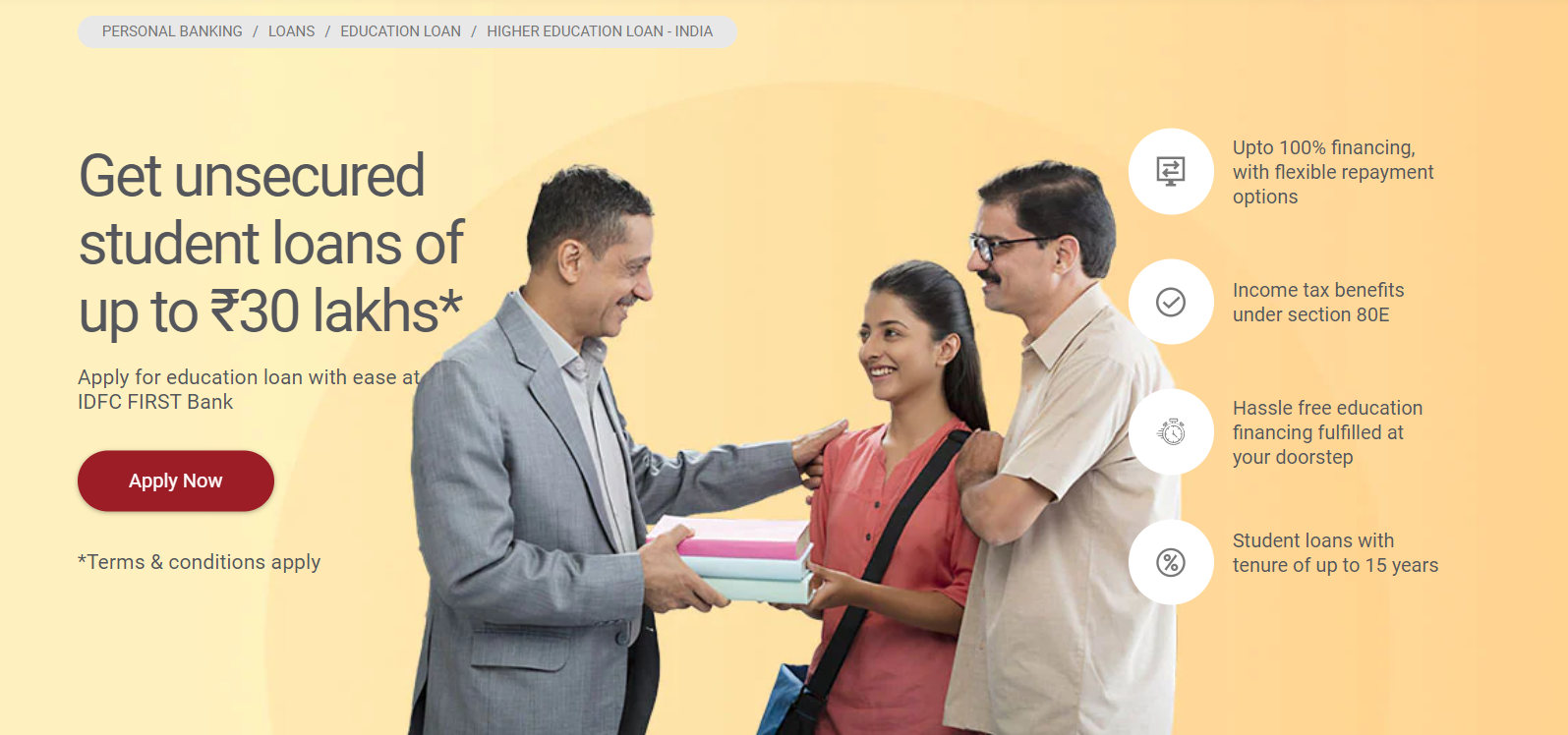

Overview Higher Education Loan - India With India, being a rapidly developing country, the demand for good quality higher education is also on the rise, to build a better future. IDFC FIRST Bank brings fully digitized and customized education loan for every student’s unique needs. Whether it is an education loan for MBA or any other professional or vocational course, part-time or full-time, our domestic student loans cover the widest range of programs. In addition to the academic expenses (tuition, hostel, exam fee etc.), our student loans provide financial coverage for additional expenses such as laptop, insurance, travel and others. Don’t let financial concerns stop you, apply for student loan today!

Eligibility Criteria

❖ Who can apply?

❖ An Indian National (Including NRI)

❖ 18 years old or above at the time of loan commencement

❖ Admitted in the desired institution after completion of the pre requisite qualifications

❖ Photo ID proof

❖ Proof of residence

❖ Passport sized photograph

❖ Proof of admission

❖ Fee structure document

❖ Salary slips of experienced candidates

❖ Academic documents

❖ Photo ID proof

❖ Proof of residence

❖ Passport sized photograph

❖ Income related documents

❖ Collateral documents

❖ Property documents

❖ FD documents

Calculator

Common Questions / FREQUENTLY ASKED QUESTIONS related to Education Loan

Will my education loan cover additional expenses, if I choose to study in India?

Yes. Apart from the college-related expenses, our student loans also cover travel expenses, purchase of computer/laptops and insurance costs.

How to apply for education loan at IDFC FIRST Bank?

IDFC FIRST Bank have simplified the procedure wherein IDFC FIRST Bank offer convenience of applying through various modes including their website, branch, mobile application and phone banking. You can even verify your eligibility for a student loan online.

Do I need a co-applicant for my education loan?

Yes, co-applicant is required to avail student loans at IDFC FIRST Bank.

I have an existing student loan with other bank. Can I transfer it to IDFC FIRST Bank?

Yes. Our Balance Transfer feature allows you to switch your existing education loan to IDFC FIRST Bank.

SBI Education Loan

Repayment period of upto 15 years after Course Period + 12 months of repayment holiday*

Processing Charges

Loans upto Rs. 20 lacs : NIL

Loans above Rs. 20 lacs: Rs. 10,000 (plus taxes)

Security

Upto Rs. 7.5 Lacs:Only Parent/ Guardian as co-borrower. No Collateral Security or third party guarantee

Above Rs. 7.5 Lacs:Parent/ Guardian as co-borrower and tangible collateral security Margin Up to Rs 4 Lacs - Nil

Above Rs 4 Lacs - 5% for studies in India, 15% for studies in abroad

Repayment will commence one year after completion of course.

Loan to be repaid in 15 years after the commencement of repayment,In case second loan is availed for higher studies later, to repay the combined loan amount in 15 years after completion of second course

The accrued interest during the moratorium period and course period is added to the principle and repayment is fixed in Equated Monthly Installments (EMI). If full interest is serviced before the commencement of repayment; EMI is fixed based on principal amount only.

Eligibility

A term loan granted to Indian Nationals for pursuing higher education in India or abroad where admission has been secured.

Courses Covered

Graduation, Post-graduation including regular technical and professional Degree/Diploma courses conducted by colleges/universities approved by UGC/ AICTE/IMC/Govt. etc Regular Degree/ Diploma Courses conducted by autonomous institutions like IIT, IIM etc Teacher training/ Nursing courses approved by Central government or the State Government Regular Degree/Diploma Courses like Aeronautical, pilot training, shipping etc. approved by Director General of Civil Aviation/Shipping/ concerned regulatory authority b. Studies abroad:

Job oriented professional/ technical Graduation Degree courses/ Post Graduation Degree and Diploma courses like MCA, MBA, MS, etc offered by reputed universities.

❖ Fees payable to college/school/hostel/Examination/Library/Laboratory fees

❖ Purchase of Books/Equipment/Instruments/Uniforms, Purchase of computers- essential for completion of the course (maximum 20% of the total tuition fees payable for completion of the course).

❖ Caution Deposit/Building Fund/Refundable Deposit (maximum 10% of tuition fees for the entire course).

❖ Travel Expenses/Passage money for studies abroad.

❖ Cost of a Two-wheeler upto Rs. 50,000/-

❖ Medical Courses: Upto Rs 30 lacs

❖ Other Courses: Upto Rs 10 lacs (Higher loan limit for studies in India may be considered on cases to case basis, maximum upto Rs 50 lacs

Upto Rs 7.50 lacs (Higher loan limit for Studies abroad are considered under Global Ed-vantage Scheme, maximum upto Rs 1.50 Crores)

Checklist of Documents to be submitted along-with duly filled Loan Application Form

- Mark sheet of 10th, 12th, Graduation (if applicable), Entrance Exam Result

- Proof of admission to course [ Offer Letter/ Admission Letter/ ID card if available]

- Schedule of expenses for course

- Copies of letter conferring scholarship, free-ship, etc.

- Gap certificate, if applicable (self-declaration from student for gap in studies)

- Passport size photographs of Student / Parent / Co-borrower / Guarantor (1copy each)

- Asset-Liability Statement of Co-applicant / Guarantor (Applicable for loans above Rs 7.50 lacs)

For Salaried Persons

(a) Latest Salary Slip(b) Form 16 OR latest IT Return (ITR V)

For other than Salaried Person

(a) Business address proof (if applicable)(b) Latest IT Returns (if applicable)

● Bank Account Statement for the last six months of Parent / Guardian/ Guarantor

● Copy of Sale Deed and other documents of title to property in respect of immovable property offered as collateral security / Photocopy of Liquid Security offered as collateral

● Permanent Account Number (PAN) of Student / Parent / Co-borrower / Guarantor

● AADHAAR (mandatory, if eligible under various interest subsidy schemes of GOI)

● Passport (mandatory for Studies Abroad)

● Submission of OVD (refer to table below)

Common Questions / FREQUENTLY ASKED QUESTIONS related to Education Loan

Where can I avail of a SBI educational loan?

You may apply for an education loan at a SBI branch nearest to the permanent residential address/ place of domicile. Additionally, for customer convenience, Scholar Loans can be availed from campus/ mapped branches.

What is the repayment schedule like?

The repayment would begin one year after the course period or six months after you get a job, whichever is earlier. You are expected to pay a minimum amount equivalent to the EMI on a monthly basis. However, you can choose to pay more than the EMI, and we do not charge any prepayment penalty.

What is EMI? How is it calculated?

EMI stands for Equated Monthly Instalments. This installment comprises both principal and interest components. Your EMI would be calculated depending on the tenor you choose, to repay your loan. The EMI would be higher if you choose to repay within a shorter period as against a longer-term loan.

A shorter repayment period, however, reduces your interest cost over the term of the loan.

Some study loans may require the borrower to begin repayment immediately after graduation, while others may offer a grace period before repayment begins. Interest rates on study loans may also vary, and some loans may offer fixed or variable interest rates.

It is important to carefully consider the terms and conditions of a study loan before accepting it, as the borrower will be responsible for repaying the loan in the future. Students should also consider other options for financing their education, such as scholarships, grants, and part-time work.

The specific criteria for study loans can vary depending on the lender and the type of loan, but here are some common factors that are often considered:

Enrollment in an eligible educational institution: To qualify for a study loan, you typically need to be enrolled or accepted into an eligible educational institution, such as a college or university.

Citizenship or residency status: Many study loans are only available to citizens or permanent residents of the country where the loan is being offered. Some loans may also require a certain length of residency or legal status.

Academic standing: Some study loans may have requirements for academic

standing, such as a minimum GPA or satisfactory academic progress. This is often the case for scholarships or grants.

Financial need: Many study loans are awarded based on financial need, as determined by the Free Application for Federal Student Aid (FAFSA) or other financial aid applications. Financial need is often determined by a formula that takes into account a student's income, assets, and family size.

Credit history: Some study loans may require a credit check or a co-signer with good credit to qualify for the loan. This is often the case for private student loans.

It is important to check the specific requirements for each loan and lender, as they may differ. It is also important to keep in mind that meeting the eligibility criteria does not guarantee approval for a loan.